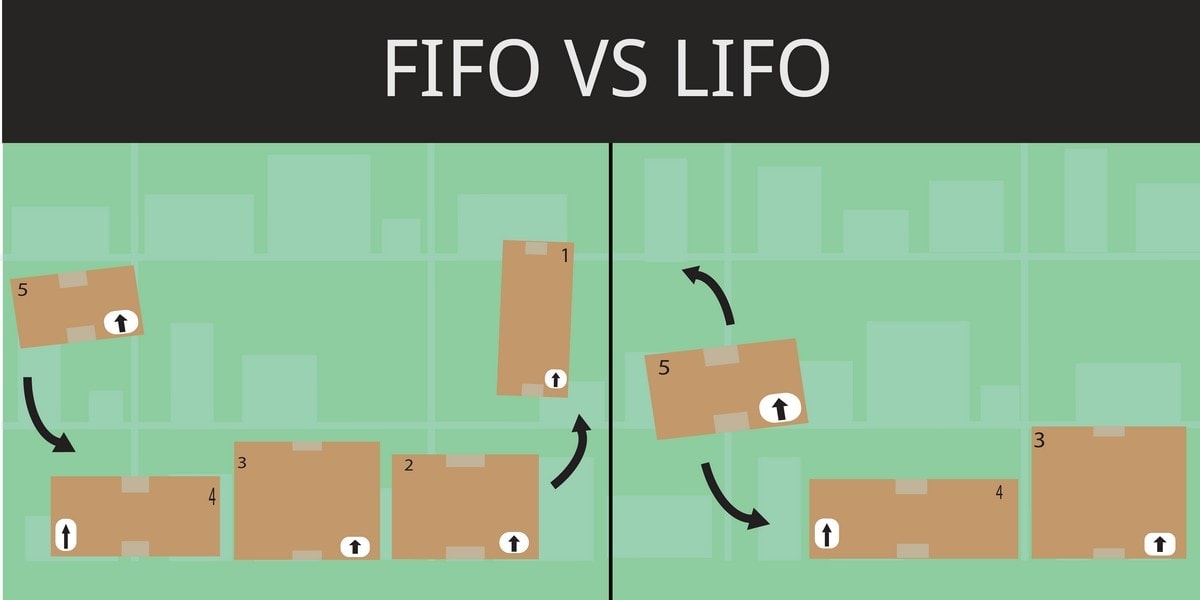

LIFO vs FIFO - Difference Between LIFO and FIFO

LIFO vs FIFO – Difference Between LIFO and FIFO

The methods LIFO and FIFO are used to determine the value of inventory unsold and all-important transactions such as the costs of goods sold, stock repurchases, etc. which are important to be reported by the end of the accounting year. the abbreviation FIFO stands for “First In First Out”.

According to this method, unsold goods are the ones which were recently added to the inventory. And LIFO stands for “Last In First Out”. According to this method, most recently added goods in the inventory will be sold first.

Therefore, Unsold goods left in the inventory are the ones which were added earliest to the inventory. However, IFRS standards don’t approve of LIFO accounting, hence, it is not very popular among industries.

However, LIFO allows lower inventory valuation during inflationary times.

Table of Contents

What is FIFO (First In, First Out)?

The meaning of FIFO is “First In First Out”, which means all the goods which were added first in the inventory will be sold first. Therefore, the goods will go out of the inventory in the same order they were first added to the stock.

The cost of all sold inventory will be equal to the total cost of oldest inventory of the stock and inventory sold on the “Profit Loss Statement” will be equal to the oldest inventory present in the stock.

The Balance Sheet will include the cost of inventory which is still in the stock and it will be treated as the latest inventory added in the stock.

What is LIFO (Last In First Out)?

The meaning of LIFO is “Last In First Out”, which means that all the goods which were added last to the inventory will be sold first. Therefore, all goods will leave the inventory in the opposite order as they have entered it. therefore, the cost of all the latest goods will be taken into consideration whenever inventory will be reported sold.

The Profit Loss statement will include the cost of latest added goods in the inventory and on the other hand, a Balance Sheet will include the cost of all the goods which are still in the stock which is equal to the oldest goods of the stock.

Example of LIFO and FIFO accounting

The example that we are going to discuss here for inventory costing and cost of goods sold can be applied to both scenarios. Assume a business which sells perfumes makes below-given purchases in one year.

Batch 1: Quantity 4000 perfumes at $8 per piece

Batch 2: Quantity 3000 perfumes at $10 per piece

Batch 3: Quantity 3500 perfumes at $12 per piece

A total of 10500 perfumes were purchased. Out of all the purchased perfumes, let us consider the company was able to sell 6000 units at $13 each. And remaining units of perfumes which are 4500 is required to be valued.

What unit cost should be used to find out the total cost of the unsold inventory? We will determine the answer to this question by using both FIFO and LIFO methods.

Using FIFO Method

In FIFP method, remaining inventory in stock is which was acquired recently. Let us assume all 3500 perfumes of batch 3 and 1000 perfumes of batch 2 are unsold. Hence the total value of unsold inventory will be (3500*$12) + (1000*$10) = $52000

The profit can be calculated using the FIFO method will be

Revenue = 6000* $13 = $78,000

Cost of Goods sold= Batch 1 (4000*$8) + Batch 2 (2000*$10) = $52,000

Profit = $78,000 – $52,000 = $26,000

Using LIFO Method

Different outcomes will be obtained using the LIFO method. The value obtained will be different because the earliest acquired goods will not be sold first. From our previous example, 4000 perfumes units from batch 1 and 2000 perfume units from batch 2 are not sold.

Hence the total value of unsold inventory will be (4000 * $8) + (1000 * $10) = $42,000

The profit can be calculated using the LIFO method will be

Revenue = 5500 * $13 = $71,500

Cost of Goods sold = (3500 * $12) + (1000 * $10) = $52,000

Profit = $71,500 – $52, 000 = $19,500

Advantages and disadvantages of LIFO and FIFO

Generally, the FIFO method of accounting is preferred more than the FIFO method as it is easy to apply in all business scenarios and also it provides better accounting.

Followings are the few advantages:

- goods can be sold and disposed of in a systematic and logical manner.

- There will be effective control of materials because of the single and uniform file flow of goods. Having control of goods which are prone to deterioration, decay, style or quality change is very important to avoid unnecessary loss.

- The countries which follow IFRS frame don’t use LIFO method as IFRS doesn’t approve of this method.

- If the LIFO method is used to manage inventory then more records are required to be kept and for long durations of time. Many companies keep at least some inventory in advance, which will require years of records.

- There are high chances that the prices of goods will be changed when they will finally be sold. Hence, this can result in huge profits or losses.

LIFO vs FIFO – Difference Between LIFO and FIFO

LIFOFIFOLIFO stands for “Last In, First Out”.FIFO stands for “First In, First Out”.Unsold inventory consists of recently acquired goods.Unsold inventory consists of oldest goods.LIFO is restricted by IFRS to implement in stores.FIFO is not restricted by either GAAP or IFRS.LIFO has bad effects of inflation.FIFO method proves to be beneficial when inflation increases.When the cost of goods rises, the purchase price recently purchased items also increases. In this way, Cost Of Goods Sold (COGS) increases with decreased profits. Income tax lowers. The value of unsold item will also decrease.When cost of goods rises, previous acquired goods were cheaper. Hence, the Costs of Goods Sold (COGS) decreases with increased profits. The income also rises and value of unsold items also increases.Keeping the record of unsold items for long year increases the burden of keeping records.Less records are required to be maintain as first came items will be sold first.There will be unusual decrease or increase in the costs of goods sold.There will be no to less chances of unusual increase or decrease in the costs of goods sold.

Comments

Related Posts

Paisa Vaisa with Anupam Gupta: Ep. 76: What's the difference between Bitcoin & Blockchain? on Apple Podcasts

Capital Markets Trends: Investment Banking | Accenture Capital Markets Blog

Responsible leadership is no longer an ESG issue; it’s a management must | Accenture Capital Markets Blog

Stocks making the biggest moves midday: Didi Global, Nvidia, PagerDuty and more

Three Types of Income